TBC Capital: a turbulent 2022 for Georgian wine exports, return to growth expected in 2023

Strategic diversification to new export markets for the Georgian wine industry has proved a fruitful – yet slow-paced – venture in recent years. But continued dependency on traditional markets like Russia and the CIS have left the industry vulnerable to regional geopolitical and economic instability. TBC Capital’s latest report looks at the industry’s tumultuous export market in 2022 and growth expectations for the coming years.

Georgian Wine Industry: International Demand

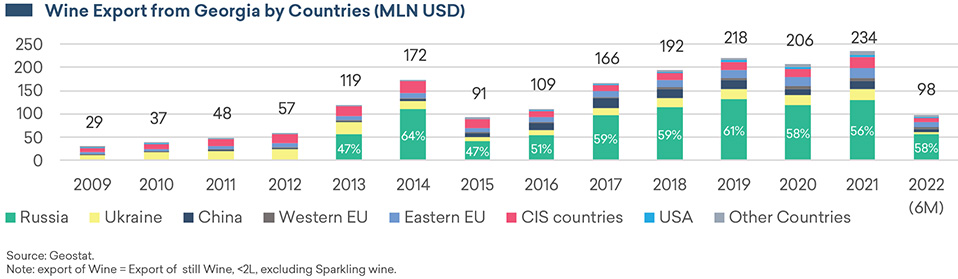

While difficult conditions like hailstorms in Kakheti affected Georgia’s grape harvest in 2021 and resulted in decreased yields, it was a banner year for wine exports. With value reaching a record $234 million, Georgian wine exports fully recovered from a 6% dip in 2020 and surpassed 2019 levels.

Despite great efforts by producers and the Georgian government to diversify export destinations, traditional markets continued to make up a significant share of exports in 2021. In addition to Ukraine, the Eastern EU, and CIS countries, which each held a respective 10% of the market last year, Russia remained the top export destination for Georgian wine, representing 56% of all exports.

The level of Russian market share in Georgian wine exports has hovered between 56% and 61% since 2017, which TBC Capital’s Vice President of Research Irina Kvakhadze says represents both a sign of progress and an opportunity for improvement. “Georgia’s wine exports are highly vulnerable to global economic and politi-cal factors. This is evidenced by the current war in Ukraine, which had a major impact on wine exports for two of the industry’s largest markets,” she notes. “However, if you look at historic trends, we do see progress. Before Russia’s embargo in 2006, the country was almost completely dependent on Russia as an export market. Since then, diversification has gradually decreased dependency on those traditional markets.”

And in lieu of traditional markets, Georgian producers have set their sights on several new target markets, including Poland, the Baltic countries, China, Japan, Germany, the UK, and the U.S. In 2021, exports to these target markets reached an all-time high of $49 million, which represented 26% of the total wine export market and a 20% increase compared to 2019.

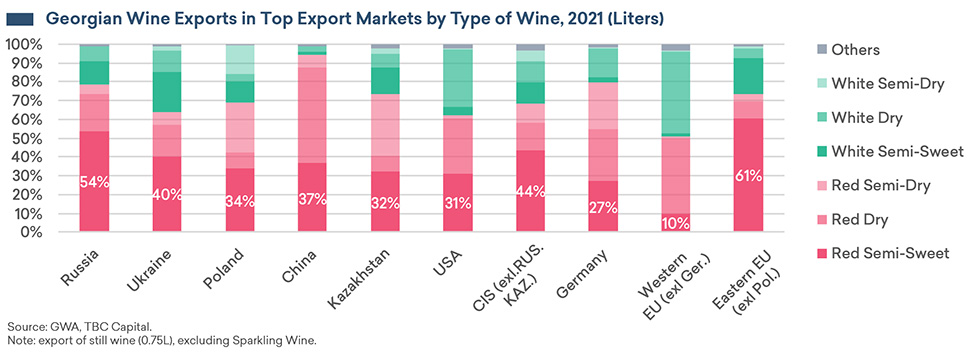

With diversified export markets has come diversified consumer preferences. Red wine accounted for 75% of exports in 2021, a favorite of traditional export markets like Russia and the CIS. However, data from 2021 shows that new target markets exhibit more diverse preferences; white dry wine made up almost one-third of wine exported to the U.S. and 43% of wine sent to Western EU markets.

Local Wine Market

Domestic consumption accounted for 24% of revenue for the Georgian wine industry in 2021. However, tour-ism remains a significant driver of demand in the local market, which is evidenced by the 43% YoY decline in domestic consumption seen in 2020 as tourism came to a screeching halt. “There is a direct correlation between tourism statistics and domestic consumption of wine,” says Kvakhadze. “We saw this when domes-tic consumption plummeted in 2020 and began to rise again in 2021 as tourism slowly returned.”

This correlation is, in part, related to the downward trend in Georgians’ wine consumption. While wine remains the most popular alcoholic drink among Georgians, data from 2021 showed that the share of Geor-gian households that consume wine was down 13% compared to 2019. Of those who do drink wine, 99% of Georgian wine consumption comes from homemade wine, meaning Georgian consumers represent a small portion of the Georgian wine industry’s customer base.

Market Projections

The first half of 2022 represented a tumultuous period for the Georgian wine industry’s export market. The Russian invasion of Ukraine decimated exports to Ukraine and left high levels of uncertainty around future trade with Russia, causing a marginal decline in total exports of wine in 1H22. Despite this geopolitical uncer-tainty, TBC Capital’s Kvakhadze says losing the Ukrainian market should not substantially impact the industry. “At the beginning of the war, our predictions for the industry were quite pessimistic,” she notes. “However, tourism levels have recovered faster than expected and increasing demand from diversified target markets and Russia have compensated partially for the loss of the Ukrainian market. Thus, we believe the wine export market will, at most, see a 5% decline in 2022 and be back to 7% YoY growth (in USD value) in 2023.”