What are financial institutions saying about Georgia’s economy?

Recent assessments from major international financial institutions, including the World Bank and the Asian Development Bank, alongside updated projections from the National Bank of Georgia, point to a common conclusion for Georgia and the wider Europe and Central Asia region: growth remains strong, but the external environment is becoming increasingly fragile.

As a highly interconnected economy, Georgia faces growing exposure to global market disruptions, weakening trade flows, inflationary pressures, and geopolitical tensions. While the country continues to outperform many regional peers, the rapid post-pandemic and post-conflict expansion of recent years is beginning to moderate.

World Bank: regional growth slows as external pressures build

In its April Europe and Central Asia Economic Update, the World Bank forecasts that growth across developing economies in Europe and Central Asia will slow to 2.1% in 2026, down from 2.6% in 2025 and 4% in 2024.

According to the bank, the slowdown reflects mounting geopolitical tensions, trade fragmentation, and continued uncertainty linked to both the war in Ukraine and instability in the Middle East. Growth in Central Asia is projected to average 4.9% in 2026–27, while Central Europe is expected to expand by roughly 2.4% this year before easing slightly in 2027. The Western Balkans are forecast to grow by 3.1%, supported by infrastructure investment and services exports, while Ukraine’s economy is expected to slow to 1.2% amid ongoing wartime pressures.

The report also warns that productivity growth across the region has weakened significantly over the past decade, leaving many economies increasingly reliant on consumption and public spending rather than investment and innovation.

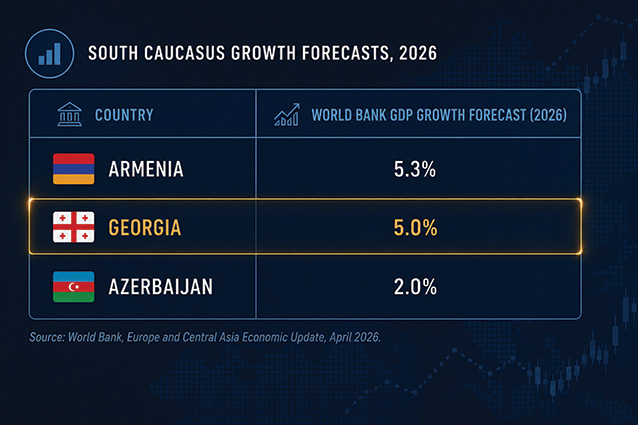

For Georgia, the World Bank slightly revised down its near-term outlook, projecting economic growth of 5% in 2026 — 0.4 percentage points lower than its previous estimate. Growth is expected to improve modestly to 5.5% in 2027.

Even with the downgrade, Georgia remains among the strongest-performing economies in the South Caucasus. Armenia’s economy is projected to grow by 5.3% in 2026, while Azerbaijan is expected to expand by just 2%.

The bank also highlighted the continued importance of re-export activity across the South Caucasus and Central Asia. In Georgia, car re-exports—primarily destined for the Kyrgyz Republic—accounted for roughly 40% of total exports and remained a major driver of trade growth. By comparison, Armenia saw exports decline for the first time since 2020 amid weaker re-exports of precious metals and stones.

At the same time, the World Bank cautioned that inflationary pressures and energy market volatility remain key risks across the region, particularly for countries dependent on imported energy, food products, and fertilizers.

ADB: Similar concerns, slightly stronger expectations

The Asian Development Bank presented a broadly similar assessment in its Asian Development Outlook 2026, although with slightly more optimistic expectations for Georgia’s economy.

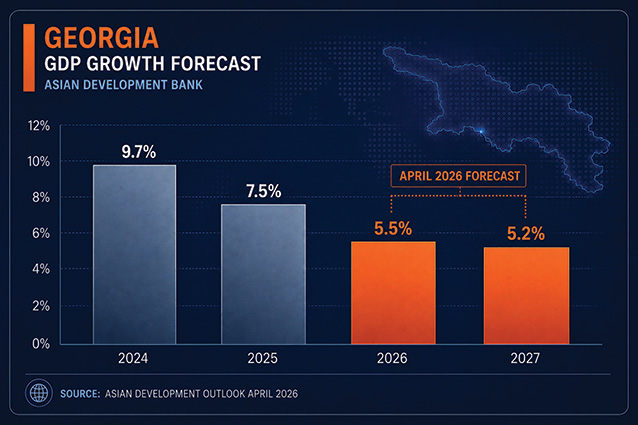

The ADB forecasts Georgia’s economy will grow by 5.5% in 2026, slowing from an estimated 7.5% expansion in 2025. According to the bank, the moderation reflects softer external demand, a weaker global recovery, and slower growth in the services sector, which has been one of the main engines of Georgia’s economy in recent years.

While services are expected to remain the primary source of growth, expansion is projected to slow considerably from the double-digit levels recorded in 2025. Industry is expected to strengthen gradually, supported by manufacturing and construction activity, while agriculture is forecasted to stabilize following contraction last year.

The bank also noted that Georgia’s current account deficit narrowed to a historic low of below 3% of GDP in 2025, although it expects the deficit to widen again as export growth moderates. Tourism and transport revenues—both major sources of foreign currency inflows—are also expected to remain vulnerable to geopolitical developments and regional instability.

At the same time, the ADB argued that Georgia retains strong long-term potential as a regional transport, trade, and logistics hub. Deeper regional integration, infrastructure investment, and improved connectivity, the bank says, could help the country move further up global value chains and sustain stronger long-term growth.

National bank sees stronger growth—and higher inflation

The latest outlook from the National Bank of Georgia (NBG) broadly aligns with the assessments of international institutions, although the central bank has taken a somewhat more optimistic view on near-term growth.

According to the NBG’s Monetary Policy Report from May 6, Georgia’s economy is now expected to grow 6.5% in 2026, up from the central bank’s previous forecast of 5%. Inflation, meanwhile, is projected to reach 4.9%, compared to the earlier estimate of 3.7%.

The upward revision follows stronger-than-expected first quarter performance, with the economy expanding by 9.1% year-on-year. However, the central bank also pointed to rising geopolitical tensions in the Middle East and higher global oil prices as major drivers behind the upward revision to inflation expectations.

The NBG warned that rising electricity tariffs and fuel costs are adding to domestic inflationary pressures. Annual inflation reached 5.9% in April — the highest level in two years — prompting the central bank to raise the refinancing rate by 0.25 percentage points to 8.25% at its May monetary policy meeting.

Taken together, the latest assessments from the World Bank, ADB, and the National Bank of Georgia suggest that while Georgia continues to outperform much of the region, the environment supporting that growth is becoming increasingly uncertain.

The country still benefits from resilient domestic demand, strong services exports, tourism inflows, and its strategic geographic position. However, international institutions are increasingly warning that sustaining high growth over the longer term will require deeper structural reforms, stronger productivity growth, and greater economic diversification as external risks continue to mount.