Mapping growth and gaps in Georgia’s logistics

Georgia has long occupied a strategic spot on the map — at the crossroads between Europe and Asia — yet turning that geographic positioning into a sustainable logistics advantage remains a complex task. TBC Capital’s latest logis-tics report highlights both the sector’s solid growth trajectory and the structural hurdles that could determine whether Georgia becomes a regional hub.

Growth anchored in trade

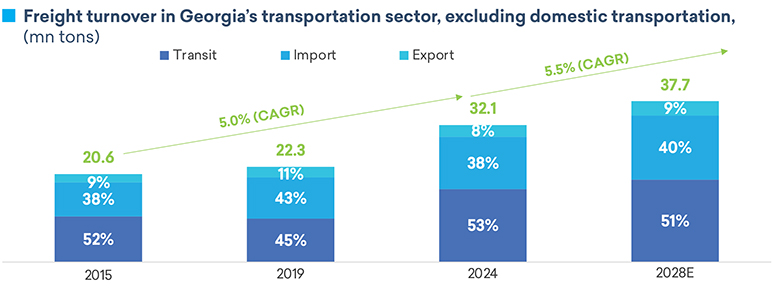

Between 2015 and 2024, cargo turnover in Georgia’s transport sector grew at a 5.0% compound annual growth rate (CAGR). Looking ahead, TBC Capital expects turnover to expand at 5.5% CAGR through 2028, underpinned by Cen-tral Asia’s rising trade flows, higher domestic demand, and steady export growth.

The logistics sector’s contribution to GDP has held stable over the past decade, moving in line with overall economic cycles. In 2024, logistics accounted for 5.9% of GDP, reflecting its role as both a transit and domestic enabler.

“Transportation and logistics have always been an important part of Georgia’s economy. As a transit country linking Europe and Asia, growth in trade flows directly drives our logistics sector,” says TBC Capital Senior Research Associ-ate Salome Deisadze.

Warehousing

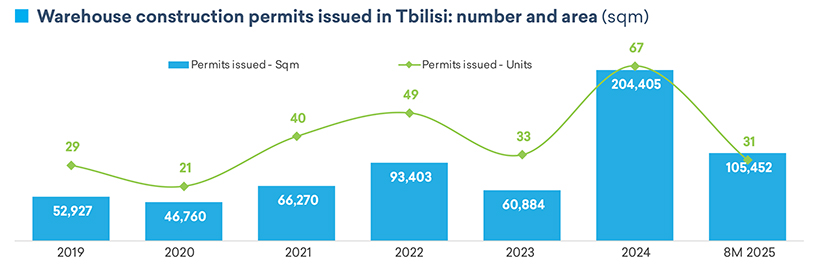

Georgia currently has around 2.2 million m² of warehouse space, of which 90% is dry storage and 10% is refrigerated. Modern facilities remain scarce—just 6% are classified as Class A— while most of the market is dominated by 1PL and 2PL operators.

Demand is accelerating, however. TBC Capital projects warehousing demand to grow at an average 9% annually through 2028, fueled by agriculture, construction materials, consumer goods, and transit flows. Tbilisi accounts for 68% of leasable warehouse space, followed by Kutaisi (17%), Poti (5%), and Batumi (5%). Rental prices range from $3–6/m² for standard space to $7–8/m² for Class A.

“High utilization — around 85% in Tbilisi — shows that warehouses are working close to full capacity,” notes Deisadze. “We saw the market respond to this in 2024 with a boom in construction permits for new warehouses.” More than 200,000 m² of space was approved in permits for the capital last year — a 3.2x increase over 2023 — and TBC Capital expects pricing to remain stable.

The Middle Corridor: strategic but strained

Georgia serves as a land bridge for trade between Europe, the Caspian region, Central Asia, and China through the Middle Corridor, where interest has been steadily increasing. In 2024, this route accounted for 4.3 million tons of cargo through the country — roughly a quarter of Georgia’s transit flows. Yet competitiveness remains an issue as the Middle Corridor trails the Northern and Southern routes in terms of capacity, cost-efficiency, and transit speed. Transport along the Middle Corridor costs $4,500–6,000 per 40-foot container, compared to $2,500–3,100 via the Northern Corridor, with transit times of 18–23 days versus 12–18 days on competing routes.

“Multimodality presents a notable challenge for Georgia’s transportation sector,” says Deisadze. “Georgia’s system depends on connecting sea, road, and rail. Modernizing the capacity of all those nodes will be essential to capitalize on new opportunities and strengthen the country’s transportation sector and transit role.”

Risks and regional competition

The recently revived Zangezur Corridor project provides an alternative connection between Central Asia, Turkey, and the EU. The route is estimated by different sources to shorten transit by 50 to 350 kilometers, while its annual capacity is projected to be approximately 15 million tons. Though unlikely in the short term, this route could redirect some Azerbaijan–Turkey and Turkey–Central Asia transit flows from Georgia. If sanctions on Russia ease, some redirected cargo is also likely to return to the Northern Corridor.

Still, demand fundamentals are strong. TBC Capital estimates that by 2030, economic growth in Middle Corridor countries is expected to nearly absorb the corridor’s full capacity, with Central Asia’s expanding trade alongside a growing population and higher consumer demand for goods and services.

“Taking into account several factors — including growing trade between the European Union and Central Asia, rising demand for minerals, the EU’s Green Agenda and Global Gateway Initiative, as well as the expanding Central Asian consumer market — we expect the Middle Corridor’s cargo turnover to reach around 9.7 million tons by 2030,” says Deisadze. She adds that planned regional infrastructure projects should raise the corridor’s capacity to 10–12 million tons by the end of the decade.

Outlook

The data underscores a dual reality: Georgia is benefitting from rising trade flows and warehousing demand, but its competitiveness depends on infrastructure upgrades, customs harmonization, and policy alignment across corridor countries. “It’s not only about infrastructure,” cautions Deisadze. “Better procedures and quality of service are essential if we want to position Georgia as a competitive transit hub.”