Sector snapshot: Batumi residential real estate

Batumi’s residential real estate market rebounded strongly in 2025, reversing the slowdown seen a year earlier and reaffirming the city’s position as one of Georgia’s most dynamic property markets, Galt & Taggart’s Batumi Residential Real Estate 2025 Review and 2026 Outlook reports. Yet beneath the headline growth, structural pressures—particularly rising supply and moderating returns—suggest a more nuanced outlook heading into 2026.

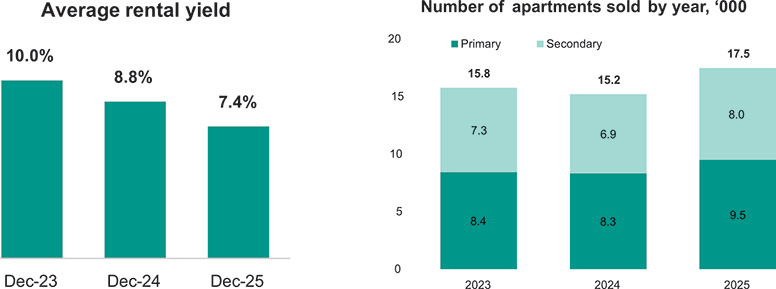

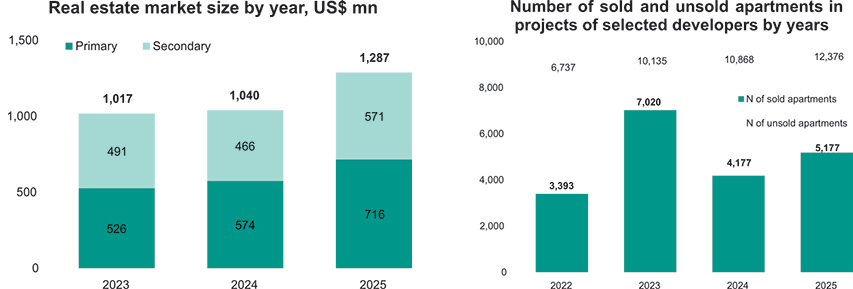

After a dip in 2024, transaction activity picked up markedly in 2025. Total apartment sales reached 17,478 units, a 15% YOY increase, while overall market size expanded to approximately $1.3 billion, up nearly 24% annually. Growth was supported by new large-scale project launches and improved activity in the secondary market, reflecting both increased housing stock and renewed buyer confidence.

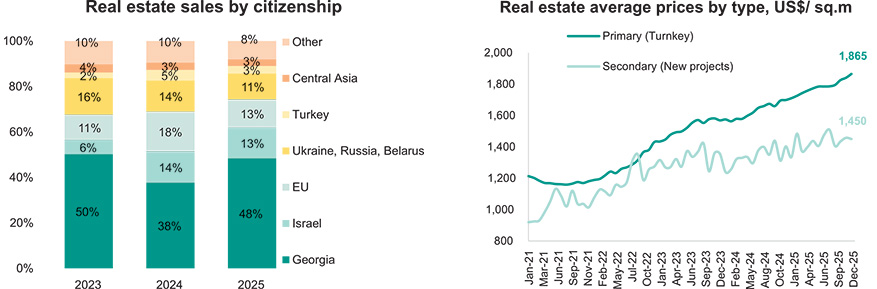

Prices continued their upward trajectory, particularly in the primary market. Average turnkey prices rose to $1,865 per square meter in 2025, up from $1,699 in 2024 and $1,569 in 2023. Primary prices also grew faster than those in the secondary market, widening the gap between the two segments. This divergence reflects both the premium positioning of new developments and the continued influx of investment-oriented projects targeting foreign buyers.

However, demand has not kept pace with supply. While sales improved, they have yet to return to peak 2023 levels, and unsold inventory continues to accumulate. By the end of 2025, unsold apartments in surveyed developer projects had risen by nearly 14%YoY, reaching approximately 12,400 units. As G&T analysts highlight, this growing pipeline underscores a key structural challenge: the market’s ability to absorb new supply.

Rental performance further reflects this imbalance. Average daily rental rates remained broadly flat at around $35.6 in 2025, despite rising property prices. As a result, rental yields declined from 8.8% in 2024 to 7.4% in 2025, compressing returns for investors. While yields remain relatively high compared to peer markets, the downward trend raises questions about the sustainability of investment-led demand.

Geographically, demand continues to concentrate in key districts. The New Boulevard area led sales activity with over 6,800 transactions, followed by the Alley of Heroes with nearly 4,000 units sold. Old Batumi remains the most premium location, with average prices exceeding $3,000 per square meter, while more affordable segments persist in peripheral zones, where prices fall below $1,500 per square meter. This segmentation reflects a market that caters simultaneously to high-end buyers, short-term rental investors, and more price-sensitive domestic demand.

Foreign buyers remain a critical driver of the market, accounting for 52% of apartment sales in 2025. Demand is geographically diverse, with notable contributions from Israel, the EU, and neighboring regions. Israeli buyers in particular have emerged as a fast-growing segment, representing 13% of total sales. While geopolitical tensions pose short-term risks to this demand stream, Batumi’s appeal as a relatively accessible and familiar destination may support continued interest over the medium term.

Looking ahead, 2026 is expected to be a year of consolidation rather than expansion. Primary market sales are projected to remain broadly flat, while the secondary market may see further growth as completed units enter circulation. Price growth is forecast to moderate to 4–6% annually, reflecting both supply pressures and a more cautious demand environment. As G&T analysts note, the pace of new supply absorption and the resilience of foreign demand will be decisive in determining whether the market stabilizes or faces further pressure.