A transit test for Georgia—can the Middle Corridor show its worth?

Iran’s closure of the Strait of Hormuz has forced East–West transit flows across Eurasia to seek alternative routes, triggering a surge in traffic along the Middle Corridor.

The Middle East crisis has triggered an unprecedented surge, not only in traffic but in international bank funding and corporate private investment along the Middle Corridor’s Europe-to-China rail and road routes. As increasing traffic is revealing some of the route’s shortfalls, the focus is increasingly on how to increase the speed of transit modernization, including at Georgia’s ports and dry cargo hubs.

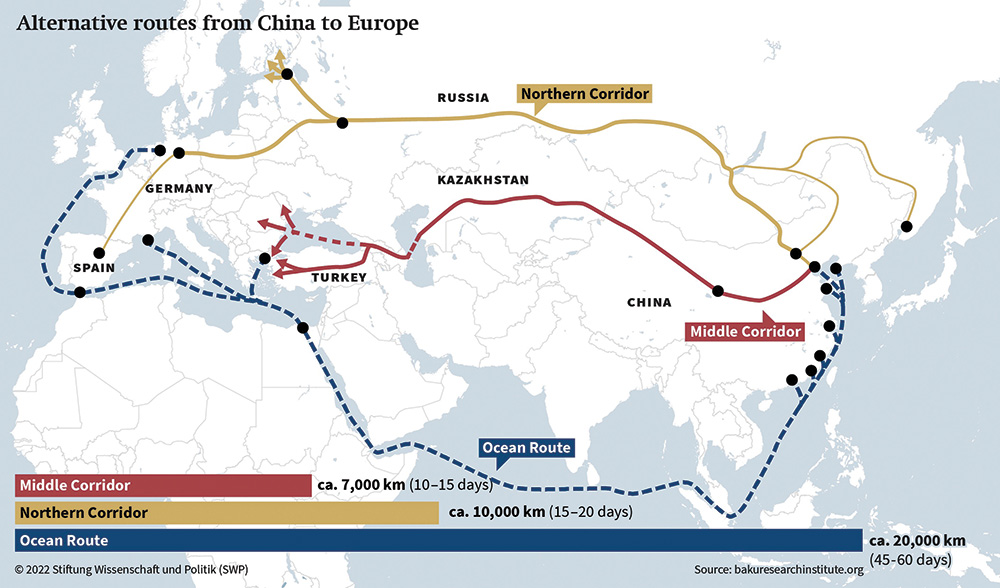

Traffic along Georgia’s E60 East–West highway reflects the growing internationalization of the Middle Corridor—also called the E60 East-West highway and the Trans-Caspian International Transport Route (TITR). Even before the Strait closed, Georgia was being criss-crossed by Russian, Turkish, Azerbaijani, Armenian, European, Georgian, Kazakh, and Chinese container lorries as its Corridor routes offer flexibility and speed and are cheaper than air.

Meredith Whitney, CEO of Meredith Whitney Advisory Group, told Bloomberg news that he saw the Middle Corridor across Georgia and Central Asia “not as a replacement for Hormuz, but as a hedge against geopolitical chokepoints from Russia to traditional trade routes.” A network of multiple reliable corridors is increasingly the strategic approach for mitigating geopolitical and supply-chain risks.

Who is driving the Middle Corridor

Washington think tank the Jamestown Foundation has published estimated market shares of the major owners of the container lorries using the Middle Corridor as 40-45% Turkish, 20-25% Kazakh, 15-20% European, and 5-10% Chinese. Kazakh operators are the fastest growing segment, it states. But the Chinese are “a rapidly emerging group,” drawn to road transport for its speed and to avoid rail bottlenecks now that many road border crossings are digitalized. China needs easy access to help find new markets for its consumer goods exports following U.S.tarriffs.

In March, the Asian Development Bank (ADB) announced a major spending spree, authorizing over $9 billion of loans to stimulate the development of the Middle Corridor. Local media ascribed the objective as smoothing the flow of energy and critical minerals. This comes shortly after it pledged up to $2.5 billion to Azerbaijan last November to support “the country’s development priorities, aimed at transforming Azerbaijan into a regional hub for connectivity, trade, and energy linking Central Asia and Europe.”

In addition, the ADB is working on a technical assistance package to modernize border crossings across Central Asia and the Caucasus. The project is designed to improve the corridor trade network by shortening border procedures.

Georgia’s accession to the Common Transit Convention in February 2025 streamlined some of the journey through its territory to Europe, as did China’s investment in multimodal logistics systems for the Middle Corridor. China and Kazakhstan have set a joint goal to increase road freight volumes via the Middle Corridor to 10 million tons by 2027, double the 2024 figure. Much Chinese Middle Corridor cargo—60% of the corridor’s total—has been carried on Kazakh-owned trailers and featured in this market share, but now Chinese logistics giants are rapidly registering new fleets of their own.

Georgian road volumes considerably exceed demand for its Middle Corridor rail services. Profits from road haulage, the most flexible transport of all and the critical “gap filler” for high value goods, have already attracted logistic players from Kazakhstan, China, and Europe as road gains traction versus air routes. These new entrants may have originally targeted transit goods seeking to bypass sanctioned routes via Russia’s North Corridor. They are now well positioned to offer door-to-door delivery in 14–18 days. This allows them to bypass volatile air routes, rising fuel surcharges, and price increases of up to 80%.

The primary maritime route for Chinese exports to Europe transits the Strait of Malacca and the Suez Canal, rather than through the Strait of Hormuz. But Middle Corridor rail freight, used largely for e-commerce goods moving from China to Europe (Poland is the entry point) has seen a sharp 31.7% YoY increase in the first two months of 2026, according to Railfreight.com.

Although up-to-date traffic figures for the bulk of the Middle Corridor’s length are not available, road transport through the Middle Corridor highways is currently enjoying a “wartime pivot” according to Abu Dhabi think tank TRENDS Research & Advisory. Kazakh news agencies report a 25% increase in truck volume in recent weeks. This, despite the numerous chokepoints along the route, such as at the Caspian Sea crossing (insufficient ferry capacity) and Red Bridge (lack of unified customs procedures). There have been long queues at Sarpi because of the weight of traffic, even though customs digitalization has reduced processing to around 40 minutes, as well as increases in fuel charges of up to 30% and collapse of standard insurance coverage.

Logistics giants in the Georgian market

Global logistics companies such as Maersk, Nurminen Logistics, CEVA Logistics, and Rail Bridge Cargo are using the Middle Corridor to bypass the northern trans-Eurasia route through Russia. The latest entrant to open in Georgia is giant German logistics group Rhenus, which has just announced a new Tbilisi office. Management board member Andreas Stockl told the press that: “With our physical presence in Georgia and comprehensive logistics services, the Rhenus Group is already fully established along the entire Trans-Caspian corridor.”

One major international logistics group handling China-Europe exports is Austria group’s Gebruder Weiss, which now has a major logistics hub in Tbilisi. It recently began a weekly dedicated truck service from China to Tbilisi, “bypassing rail schedules to provide faster delivery.” It has several Chinese JV partners, including Global Freight System (GFS) China, Jilin International Transport Corporation and Jebsen Group. In the e-commerce and retail sector, it acts as a fulfillment and logistics partner for several major Chinese entities.

The Kazakh and the Chinese companies who can be observed in Georgia’s logistics market have taken different approaches. Kazakhstan’s approach has been to focus on joint infrastructure and digital integration, while China has established a more direct presence through private commercial hubs and extensive freight forwarding networks.

Kazakhstan has invested in both “soft” and “hard” infrastructure. Its principal investment has been in building the Poti Container Terminal and establishing the Middle Corridor Multimodal, along with railway operators from Georgia and Azerbaijan (with China joining late last year). The latter aims to streamline freight transport (both rail and road) between Asia and Europe by providing “one-stop-shop” logistics services, handling everything from documentation to transit management across multiple borders. The venture should increase traffic by automating customs procedures and documentation through shared digital platforms, significantly reducing border delays.

There are many Kazakh companies operating trucking businesses. One is the country’s rail-focused national rail group: it has a subsidiary, KTZ Express, which manages intermodal services along the Middle Corridor, but it partners with European firms for “last minute” trucking. Others include private operator Globalink Logistics Group, which provides comprehensive road freight, project logistics, and customs brokerage across the CIS and Europe. Pandora Logistics, CK Logistics, and InterLuxCargo are others in the logistics sector.

Unlike the Kazakh entities, several Chinese-linked logistic companies and services operate directly on the ground (including some among the 1,900 Chinese companies registered in Georgia, a record 291 registering last year), many doing local and regional business.

The major expansion of use of the Middle Corridor by China’s logistic groups carrying high-value and e-commerce goods began in 2024, according to the IRU, driven by the need for alternatives to the Northern Corridor and the Red Sea crisis (fears of Houthi attacks). This forced shippers to seek faster, more secure routes and they established footprints in Europe, including making heavy investments in logistics infrastructure, such as warehousing and parcel locker networks, particularly in Central and Eastern Europe.

While Chinese state-owned enterprises are investing in the rail and maritime infrastructure of the Middle Corridor, private and semi-private firms handle road transport operation, according to the IRU’s intelligence platform. It adds that “Chinese companies are increasingly using road transportation (trucking) to move goods directly into Europe, bypassing traditional ocean freight for faster delivery times, particularly for high-value goods like electronics and electric vehicles.” Some Chinese logistics providers are also extending the trans-Asia road corridors to manufacturing hubs in Vietnam and Cambodia, linking Southeast Asia with European markets via Central Asia.

In Georgia, Chinese-founded or partnered firms, like MyChina.ge, WORLDLOG & SILKPOST (offering 20-day groupage delivery from China to Georgia) and BetterLuckShipping, provide door-to-door container trucking and warehouse consolidation services specifically for the China-Georgia route. At the top end of the corporate scale, major industrial holding company Hualing manages the large logistics hub in Kutaisi’s Free Industrial Zone and facilitates truck distribution of Chinese goods across the Caucasus.

Pressure to scale

As the increased traffic exposes bottlenecks on the Middle Corridor, regional governments are being forced to abandon slow-moving national projects in favor of unified regional strategies. To address four-day customs delays, for example, Azerbaijan, Georgia, and Kazakhstan are now prioritizing the harmonization and digitalization of transit documents, according to Trends.

While Georgian road trucking numbers overall dipped last year (down 4.5%), they have been observed to be recovering fast in recent weeks, due to the Middle East crisis. Even in 2025, the Middle Corridor containerized portion of this traffic increased dramatically, rising by 170% in H1. This is a very useful income for the Georgian government, with lorry fees at GEL 350 each bringing in GEL 171 million in 2025, and GEL179 million in 2024.

Georgia aims to finish work on key Middle Corridor highway sections by the end of 2026, including the Rustavi-Red Bridge (Azerbaijan border), Algeti–Sadakhlo (Armenia), and Batumi–Sarpi (Turkey)—according to Azernews.Az. That means the last unfinished link of the international route along the Black Sea coast, critical for trade and tourism, will thus be completed.