Georgia’s economy in focus: growth projections improve amid global uncertainty

Forecasting Georgia’s GDP is not easy, given the economy’s cyclical patterns, high level of informality, and small size—which makes it particularly sensitive to external shocks. Nonetheless, the major international institutions and financial market analysts tracking Georgia have revised their 2025 economic growth projections upward, with most now estimating growth of around 7% for the year.

These upward revisions reflect strong recent economic performance—particularly in the first half of 2025—driven by dynamism in tourism, the ICT sector, and transit transport, along with solid macroeconomic fundamentals such as reserves and debt levels. Confidence from major institutions including the IMF, World Bank, and ADB has reinforced this trend. The average economic growth forecast for Georgia for 2025–2027 now stands at 5.8%, almost double the average for other EU candidate countries. However, analysts continue to note that structural risks and exposure to external shocks remain key challenges.

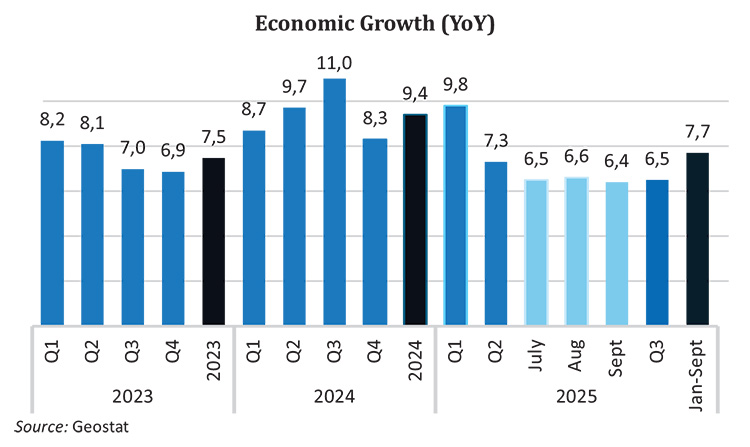

Despite an unfavorable external environment and geopolitical tensions, the Georgian economy recorded an average growth rate of 9.7% between 2021 and 2024. In 2021-2022, double-digit economic growth was observed at 10.6% and 11.0%, respectively. Growth continued in 2023 at 7.5%, and preliminary estimates indicate that the economy expanded by 9.4% in 2024. In the first half of 2025, estimated growth reached 8.3%, supported in part by structural shifts underpinning sustained high growth.

Regarding longer-term GDP forecasts, the IMF—and most other major forecasters—expect growth to moderate toward 5% in the coming years. This caution reflects belief that much of the 2025 outperformance is cyclical or driven by short-term factors (e.g., demand and tourism).

Upward revisions in GDP forecasts from leading institutions

- International Monetary Fund: Increased its 2025 growth forecast from 6% to 7.2%.

- World Bank: Raised its 2025 growth forecast to 7%, citing stronger-than-expected 2024 performance.

- Asian Development Bank: Increased its 2025 forecast to 7%.

- National Bank of Georgia: Revised its 2025 GDP growth projection to 7.4%.

- Fitch: Raised its 2025 GDP forecast to 5.6%.

- S&P: Increased its 2025 forecast to 7.1%, up from 5.7%.

- Galt & Taggart: Projects 7.5% real GDP growth in 2025.

- TBC Capital: Forecasts real GDP growth at 7.3% in 2025.

- ISET: July 2025 projection (from May data) estimates around 7.1% in the base scenario.

International Monetary Fund

The IMF reports that the Georgian economy has performed strongly despite domestic and geopolitical uncertainty. In the IMF Executive Board report following its 2025 July consultation with Georgia, it notes:

The Georgian economy has performed remarkably well despite elevated domestic and geopolitical uncertainty. Annual growth has averaged over 9 percent since 2021, headline inflation has returned to target after undershooting for two years, and public debt declined to 36% of GDP in 2024.

Looking ahead, growth is projected to ease to 7.2% in 2025 driven by resilient domestic demand and continued strength in tourism, information and communication technology (ICT), and transport (transit trade) and then in the following years converge to its medium-term potential of 5% as domestic demand decelerates.

The IMF report notes that inflation is projected to remain near the 3% target, and the current account deficit is expected to stabilize around 5% of GDP. Reserves are projected to improve gradually, supported by opportunistic foreign exchange purchases and a recovery in foreign direct investment. The external position in 2024 was broadly in line with the level implied by fundamentals and desirable policies.

It notes that since 2021, real GDP growth has averaged over 9% annually, driven by a strong post-pandemic recovery and sustained expansion in ICT and transport services sectors, supported by immigration, financial inflows, and transit trade linked to the war in Ukraine. These trends have boosted per capita income and reduced unemployment and poverty. Inflation has remained low, aided by tight monetary policy and a strong lari, while public debt returned to pre-pandemic levels. However, challenges persist due to high structural unemployment, income inequality, outward migration, and informality.

The IMF sees risks to the outlook as broadly balanced, amid high global uncertainty and political tensions. It notes that a resolution of the war in Ukraine may reverse some gains from migration and transit trade, but greater regional stability and reconstruction could offset these effects.

Finally, it notes that direct exposure to global trade tensions is limited, given Georgia’s low export share to the U.S. and exemptions for key products. However, indirect effects from weaker investor sentiment, slower trading partner growth, or supply chain disruptions could weigh on exports and raise import costs. Georgia might benefit from lower oil prices and increased trade diversion. Domestically, heightened political uncertainty and potential sanctions could dampen FDI, tourism, and pressure the lari. In this case, the IMF says, Georgia’s fiscal and financial buffers would help cushion adverse shocks.

World Bank

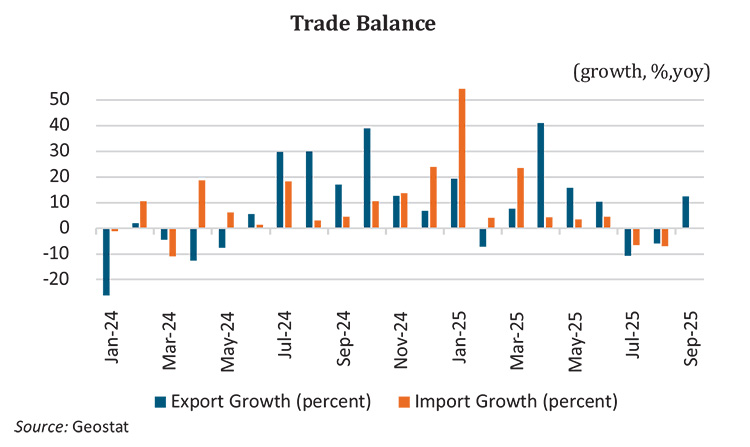

The World Bank’s updated forecast projects Georgia’s economic growth at 7% in 2025, 1.5 percentage points higher than its June projection. Growth of 5.5% is expected in 2026, marking a 0.5-point upward revision. According to the World Bank, Georgia is set to record the highest average economic growth among European countries between 2025 and 2027. It notes that the current account deficit widened to 8.6% of GDP in Q1 2025, reflecting weaker exports of goods and lower remittances, partly offset by strong service exports. In H1, goods exports grew by 13.7% YoY, driven by re-exports. Remittances increased by 3.6% YoY, while tourism receipts grew by 3.8% YoY. FDI inflows remained subdued at 2% of GDP in Q1. The lari appreciated by 0.5 % YoY against the USD by end-July, while reserves increased by 7.5% YoY, reaching 3.2 months of imports.

Asian Development Bank

The ADB updated its forecast in September, projecting 7% growth in 2025—one percentage point higher than in April—and 5% growth in 2026. The bank estimates that Georgia’s real growth in the first half of 2025 was 8.3%; the services sector increased by 12.9%, mainly driven by a 28.6% growth in the ICT sector. Vehicle re-exports, a key source of foreign exchange, grew by 30.3%. However, a 25% U.S. tariff on imported vehicles introduced in April 2025 may raise prices for second-hand U.S. vehicles, potentially reducing Georgia’s re-exports. But growth in services—particularly in tourism, transport, and information technology—is expected to offset any future slowdown in merchandise exports. Tourism revenues grew at 3.8%, building on record-high receipts in 2024, while overall service exports expanded by 10.2%, reflecting Georgia’s emerging role as a key transit route for Trans-Caspian trade and cargo movements. Higher U.S. and European transfers helped increase remittances by 3.5% in H1—despite a 26.5% drop in transfers from Russia. Foreign direct investment (FDI) declined by 7.7%, mainly due to weaker investment outside information and communication, though the share of reinvested FDI remained high at 83.6%.

European Bank for Reconstruction and Development

According to the EBRD’s updated September forecast, Georgia’s economic growth for 2025 will be 7%—one percentage point higher than the bank’s May forecast—and 5% for 2026. It states that economic expansion is supported by increased lending and significant growth in the information technology and education sectors. It estimates that Georgia will have the highest average economic growth among European countries in both 2025 and the 2025-2027, with figures double those of other EU candidates. After 9.4% growth in 2024, the economy expanded by 8.3% in the first half of 2025. Tourism resilience continues to support fiscal and external balances, while reserves have increased to $5.2 billion, covering over three months of imports.

European Commission

The European Commission’s Autumn 2025 Economic Forecast anticipates growth exceeding 7% in 2025, moderating to 5–5.5% in 2026 and 2027. Growth is projected to be driven by private and government consumption, while investment is set to slow down on the back of weakened business confidence and domestic political turmoil. The unemployment rate is set to slightly decline by 2027, while remaining structurally high. Inflation picked up in 2025 due to rising food prices, but price pressures are expected to ease going forward. The general government deficit is set to remain limited over the forecast horizon, just above 2% of GDP, while public debt is expected to decline towards 35% of GDP.

National Bank of Georgia

After strong growth of 7.7% in the first three quarters of 2025, the NBG expects the economy to moderate toward its 5% potential in 2026. Earlier in 2025, the bank had revised its GDP growth forecast to 7.4%. Average inflation is projected at around 4% in 2025, falling to 3.5% in 2026. Inflation stood at 5.2% YoY in early November, primarily driven by food prices—which it expects to be temporary and not cause widespread price increases. The NBG considers current monetary policy moderately tight, keeping the refinancing rate at 8% in November, and notes readiness to adjust policy based on future data and risks.

Standard & Poor’s Due to higher-than-expected current economic growth, S&P has raised its 2025 forecast for Georgia to 7.1%, up from 5.7% at the beginning of the year. The forecast for the current account deficit has also improved and is now expected to be 4.1% in 2025, instead of the previously projected 5.0%. The rating agency views Georgia’s fiscal and monetary policy framework as relatively prudent and forward-looking in the regional context, attributing this to structural reforms, which it says have contributed to an improved business environment. However, the agency notes that elevated domestic political uncertainty, the suspension of Georgia’s EU accession process, and the shifting dynamics of its relationship with Western partners could weigh on medium-term growth prospects and further weaken FDI inflows. It anticipates a decline in capital formation, largely attributed to the increased political uncertainty and the EU’s decision to suspend Georgia’s accession process.