TBC Capital || Global recalibration, local resilience: what 2026 holds for Georgia’s economy

After years of global volatility, 2025 proved more resilient than anticipated. TBC Capital forecasts that 2026 will bring slower but more sustainable growth, easing inflation, and gradual monetary policy normalization world-wide, as Georgia shifts from exceptional post-pandemic expansion toward a more balanced growth trajectory.

Global trends

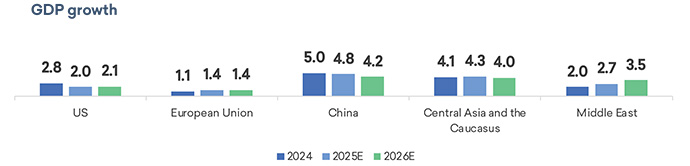

Global economic growth is set to normalize in 2026 following a stronger-than-anticipated 2025. Growth in the United States, the European Union, and China is projected to moderate, while Central Asia and the Caucasus and the Middle East continue to demonstrate relatively stronger growth dynamics.

Inflation trends are moving downward. In both the U.S. and the EU, inflation is normalizing as elevated policy rates have achieved their intended effect, while dynamics remain more uneven across emerging regions. As price pressures ease, central banks across developed markets are entering a phase of monetary policy easing. TBC Capital antici-pates rate cuts across major economies through 2026, marking a shift after an extended post-COVID tightening cycle.

Energy markets are also undergoing a structural shift. After several years of tight conditions, the oil market is likely to move into a supply-led environment in 2026, with projected net supply growth of 2.5–3.0 million barrels per day. As a result, oil prices are forecast to remain capped throughout the year, despite continued sanctions on Russian exports.

Reflecting on the global outlook, TBC Capital’s Senior Analyst of Global Capital Markets Rati Tsiklauri notes that 2026 is likely to be defined less by acceleration and more by normalization. “After the strong overperformance of 2025, 2026 is really about normalization—growth will continue, but at a more measured and sustainable pace,” he says. “In the United States, we still see positive economic growth in 2026, supported partly by the ongoing AI investment cycle and large-scale capital expenditures.”

Tsiklauri also points to growing divergence across regions, with uneven growth in Europe, improving domestic focus in China, and selective strength across emerging markets.

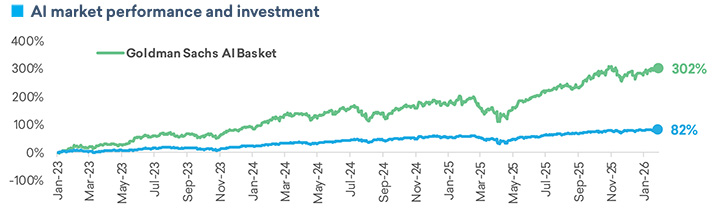

Beyond cyclical trends, structural forces continue to reshape the global economy. Trade regimes are fragmenting, with U.S. tariffs imposed across a wide range of goods and industries, while efforts to resolve the Russia–Ukraine war could have far-reaching implications for global markets. At the same time, artificial intelligence remains a dominant investment theme. Since the start of the AI boom in late 2022, Goldman Sachs’ AI-focused equity basket has tripled in size, supported by rising capital expenditures and expectations of potential 20–30% productivity gains over the medium term.

Georgia: Growth moderates, but outperformance remains

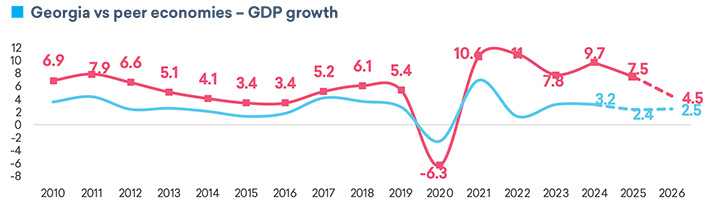

Against this global backdrop, Georgia’s economic outlook for 2026 remains favorable. After recording 7.5% GDP growth in 2025, economic expansion is projected to moderate to 4.5% in 2026, while still outperforming most peer economies.

Consumption has been the dominant driver of growth in recent years and is set to remain the primary contributor in 2026. Inflation accelerated in 2025, driven primarily by higher food prices. End-period inflation reached 4.0% in 2025 and is forecasted to slow toward around 3.5% by the end of 2026, moving closer to the National Bank of Georgia’s target. Monetary policy is likely to remain cautious, with the policy rate projected to decline from 8% at end-2025 to 7.5% by end-2026.

Exchange rate stability and external buffers

The lari is likely to weaken only marginally against the U.S. dollar in 2026, supported by an improved external balance, a real effective exchange rate below its long-term trend, and stable monetary conditions.

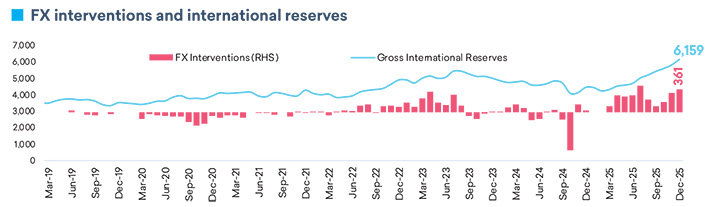

Foreign exchange reserves will provide an additional buffer. In 2025, the National Bank of Georgia purchased nearly $2.5 billion on the FX market, lifting gross international reserves to a historically high $6.2 billion by the end of December.