TBC Capital || Georgia’s infrastructure pipeline expands amid cost pressures

Georgia’s infrastructure sector is entering a new phase—one defined by rising public investment, evolving procurement rules, and moderating but still elevated construction costs. TBC Capital’s latest overview highlights a strong pipeline of large-scale projects, alongside shifting execution dynamics as regulatory changes and cost pressures reshape the sector.

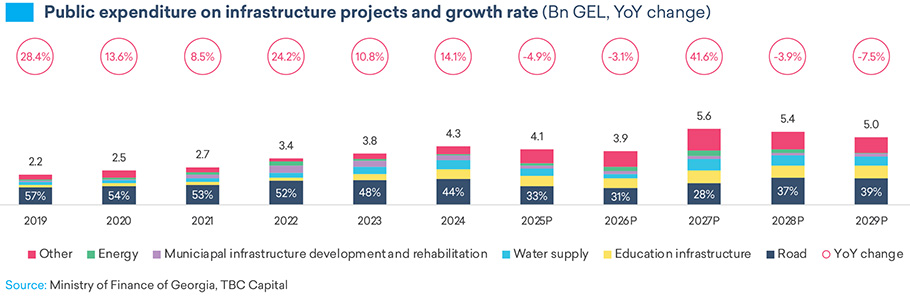

Public capital expenditure has expanded significantly in recent years, rising from GEL 2.2 billion in 2019 to a projected GEL 3.9 billion in 2026—an increase of nearly 78%. The sector continues to be driven primarily by large-scale projects, including highways, roads, bridges, water systems, and public facilities, underscoring infrastructure’s central role in Georgia’s develop-ment strategy.

While overall investment remains strong, 2025 saw some short-term disruptions. A number of projects were temporarily delayed due to ongoing changes in infrastructure financing frameworks, including revised procurement procedures and approval processes.

Road infrastructure remains the largest component of public capital spending, projected to account for approximately 31% in 2026. Education and water infrastructure follow as the next largest segments, reflecting continued investment in both transport connectivity and public services.

Procurement Reforms Reshape Execution

A key factor influencing the sector is the ongoing reform of Georgia’s public procurement framework. Changes introduced in 2025 and further refined in early 2026 have updated procedures for planning, documentation, and tender execution.

The reforms include new requirements around tender timelines, expanded thresholds for simplified procurement, and changes to competition notices. Market research rules have also been adjusted to provide greater flexibility for smaller procurement processes, while electronic systems are being introduced to streamline procurement workflows.

These changes have contributed to temporary delays as institutions and contractors adapt to the updated system. As TBC Capital Senior Associate Salome Deisadze explains, “This uncertainty had a short-term impact on the sector, contributing to delays in project implementation and reduced demand for construction materials. However, we view these effects as temporary, with the expectation that project activity will normalize as market participants adapt to the updated procedures.”

At the same time, the reforms introduce more structured requirements for participation. Deisadze notes that “One of the more significant changes is the introduction of revised collateral and guarantee requirements for participation in tenders, which are now more structured and linked to project value.”

These adjustments may influence participation dynamics, particularly for smaller contractors, while also shaping pricing strategies and liquidity planning across the sector.

Costs Stabilize at Elevated Levels

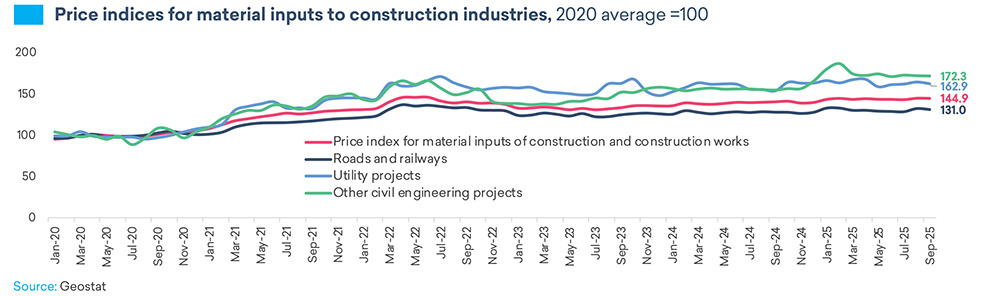

Construction input costs, which rose sharply between 2020 and 2022 due to global supply disruptions and rising energy prices, had begun to moderate since late 2023, but remained above pre-pandemic levels, continuing to shape project economics.

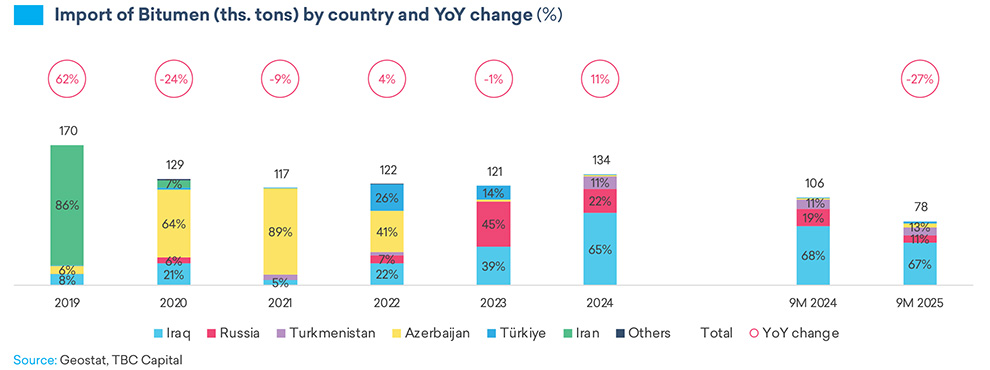

Bitumen, a critical input for road construction, has closely followed global crude oil price trends. While prices had moderat-ed from earlier peaks, they remain structurally higher than pre-2020 levels. More recently, the outbreak of war in the Middle East at the end of February has introduced renewed volatility into global energy markets. This is expected to place addition-al upward pressure on construction material prices—particularly bitumen—while the duration and magnitude of this impact remain uncertain.

As Deisadze explains, “Bitumen prices largely follow global crude oil trends. While there had been some moderation, ongo-ing geopolitical tensions—particularly in the Middle East—are contributing to uncertainty and limiting the potential for prices to decline further.”

Outlook

The data points to continued high levels of infrastructure investment, supported by sustained demand for connectivity and public services. At the same time, execution dynamics are evolving, shaped by procurement reforms and cost considerations.

As Deisadze notes, the sector’s trajectory remains closely tied to public spending: “Our outlook for the infrastructure sector is closely tied to public capital expenditure, which remains the primary driver. Based on current projections, we expect spending to broadly follow planned levels in the coming years.”

She adds that cost pressures remain a key variable: “In addition to rising prices of construction materials, there is additional potential for upside pressure on expenditures, as rising crude oil prices feed into higher transportation and logistics costs, including fuel and insurance, further increasing overall project costs.”

For contractors and investors, the sector continues to offer opportunities across transport and municipal infrastructure. However, navigating regulatory adjustments and managing cost structures will remain central to project delivery in the near term.