Foreign capital finds comfort in Georgia’s numbers

“Investment is a numbers game.” So goes the maxim, and currently there seem to be plenty of numbers in Georgia’s favor in the eyes of overseas investors, whatever the country’s challenges. Foreign investment funds are again buying Georgian government bonds, and not only those issued in euros. Local currency ones—lari-denominated Georgian government Treasury bonds—seem to have positively leapt back into favor.

Having secured an internationally recognized benchmark for evaluating Georgian risk and yield on key U.S.-based bond trading platforms such as Bloomberg and the Intercontinental Exchange (ICE), Georgia is now looking east, taking steps to unlock access to what could become a significant new source of international capital: China’s financial markets.

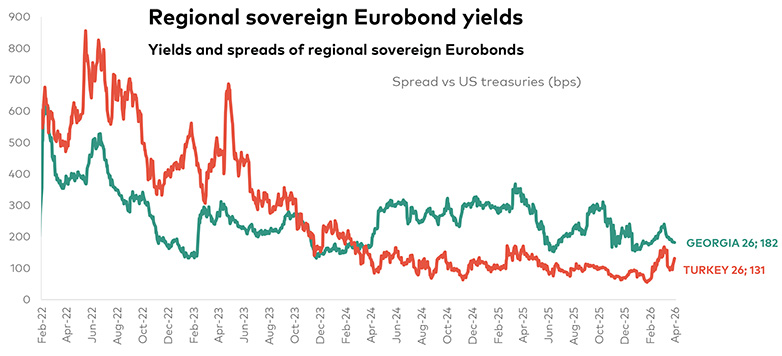

Amid the global financial market chaos brought by wars in the Middle East and Ukraine, inflation-priming oil price shocks, Trump tariffs, and the AI battleground, Georgia has been looking all year like a relatively safe and stable haven for international funds—and one offering competitive yields. In 2026, Georgia has thus far outperformed the broader J.P. Morgan NEXI (Next Generation Emerging Markets) Index. So, it is doing much better than its peers.

As an indication of Georgia’s yield attractions, in early May the Ministry of Finance issued benchmark local currency bonds (approximately 2.8 years remaining maturity) with a weighted average yield of 8.345%. By comparison, the 2-year U.S. Treasury note was yielding 3.90%, and the 10-year note 4.38%.

The first sign of Georgia’s 2026 financing success was January’s five-times-plus oversubscribed new 5-year government €500 million Eurobond, with $2.8 billion raised for a bond rollover with a coupon of 5.125%. Encouraged by the obvious popularity of Georgian notes, foreign investors were then reported the following month to be participating in domestic bond auctions—including a 3-year GEL 40 million Treasury note, which was oversubscribed 4.7 times.

Since then, the government has been able to auction on steadily improving terms. Although no details have been announced by the Ministry of Finance, recent auction data from April and early May show that Georgian government securities have continued to attract strong demand. With demand consistently exceeding supply, and the government able to continue lengthening maturities, brokers suggest that foreign interest is continuing, although the majority of buyers remain local, primarily banks.

Georgia’s €500 million Eurobond might seem too small to be noticed in the global €21 trillion Eurobond market, but the entry to ICE and Bloomberg helped create confidence by providing an internationally recognized benchmark for evaluating risk and yield. And investment funds are desperate for yield. The revived foreign interest in Georgia has helped allay fears that the government’s money market funding needs for its huge infrastructure bill would fall on local banks, crowding out private sector lending.

The list of blue-blooded international frontier and other funds that bought the Eurobond is impressive. Lead managers of the Eurobond issue included U.S. investment banking giants JP Morgan and Citi, as well as Europe’s Société Générale. Major investment groups now reporting that they hold Georgian assets in their emerging market bond funds include Vanguard, BlackRock, Ashmore, and PIMCO. The Georgian Ministry of Finance reported an investor breakdown in the Eurobond issue as 38% UK-based, 34% U.S.-based, 23% Continental European, and 5% Middle Eastern and Asian.

Reinforcing January’s display of confidence, international credit rating agency S&P affirmed a “stable outlook” for Georgia the following month, citing strong fiscal performance and foreign currency reserves. Georgia’s reserves were at a record high of $6.65 billion as of February, thanks to the soaring value of its gold holdings and the central bank’s active accumulation policies.

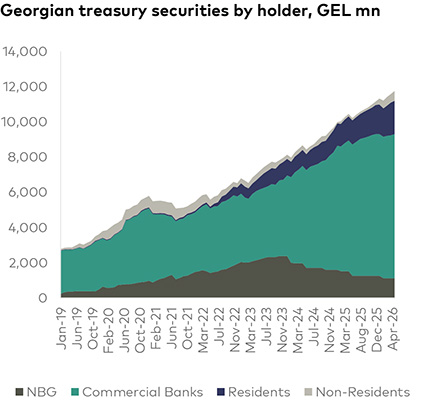

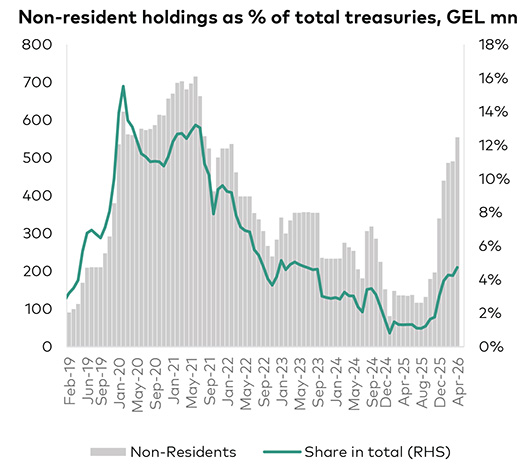

For Georgian lari treasury bonds, the numbers show that interest from foreign investors was experiencing a strong revival in early 2026. Foreign buying had plummeted over the last few years, dropping from a 2019 peak of 16% of the total market to 1% in 2025, according to Galt & Taggart and the National Bank of Georgia (NBG). But this year, buyers have so far taken the percentage back up to more than 4%.

The growth story investors are buying

Among Georgia’s attractive qualities for foreign investors is an economy growing at a rate above forecasts—due in part to the ongoing move of a large number of state enterprises into the private sector. The government’s strategy is to get these assets off its books, reducing government debt—a commitment it has made to the IMF. Some state property and enterprises have been taken over by major private groups, and some water utilities may struggle to thrive without subsidized government loans and be forced to increase tariffs. But Georgia Rail, Georgian Oil & Gas, and others have sufficient foreign income to service cheap foreign currency loans and can borrow without needing the government to on-lend.

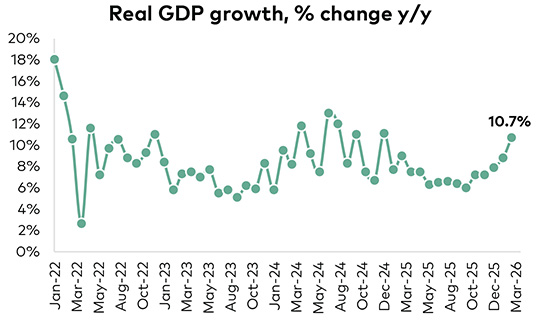

The rise in average GDP growth to 9.1% in Q1 came from a mixture of factors, partially as a result of transit cargo rerouting and warehousing demand because of disruptions to shipping in the Strait of Hormuz. There was also rising demand for copper, ferroalloys, refined oil products, and fertilizers, as well as increased production in the wine and water sectors. Heavy infrastructure development also contributed as the government spent on road projects and work progressed on hydroelectric and wind power plant construction. Foreign investors were pleased to see industrial development leading, even as tourism’s contribution declined as the escalating Middle East conflict reduced the number of high-spending tourists from Israel and Iran.

Longer-term concerns about Georgia have by no means been entirely dismissed by foreign funds. But while the “underlying” Georgian story may look fragile to locals and political analysts, investors, as local brokers observe, often decide to be pragmatic. They look at solvency rather than social harmony, and even with recent spending and prospective infrastructure bills, Georgia’s debt-to-GDP ratio of 39–40% remains lower than that of many of its peers.

Markets looking past domestic politics

Several analysts have argued that investor sentiment could become more materially affected if developments were to directly impact Georgia’s financial system or international standing. One London-based fund manager suggested that measures targeting the banking sector or major state entities would likely attract greater market attention, while commentators writing for BNE Intellinews have pointed to scenarios such as the suspension of Georgia’s EU candidate status as potentially significant. Others have noted that placement on the G7-backed Financial Action Task Force (FATF) “gray list”—officially known as Jurisdictions under Increased Monitoring, which identifies countries with strategic deficiencies in combating money laundering and terrorist financing—could also influence investor perceptions.

Countering sanction fears, the NBG has implemented several layers of defense to protect the banking sector. It has a dedicated unit to monitor international sanctions compliance and conducts on-site inspections of commercial banks. Moreover, Georgian banks have consistently ceased operations with sanctioned Russian payment systems such as Unistream. In April 2026, the NBG updated regulations to impose heavier fines on any financial participant found facilitating sanctions evasion. Major banks such as TBC and Bank of Georgia maintain such high compliance standards, in part to preserve their Western stock listings, that, as Reuters notes, investors feel the financial core is safe even if the trade borders are porous.

Investors such as U.S. giant BlackRock may be unhappy about the passage of the “Offshore Law,” which they said was designed to evade potential sanctions. Their concern was compliance with ESG and risk mandates. Balancing these concerns, however, are positives that include the tight fiscal discipline maintained by the Ministry of Finance, with the budget deficit remaining below 3% of GDP, signaling to markets that the machinery of the state is still functioning effectively.

Markets tend to trust ministries of finance and revenue services more than parliaments, valuing the continuity of bureaucracies. The massive growth in Georgian real estate and services has created a very comfortable tax revenue cushion.

Investors no longer see the influx of IT workers as a “temporary” blip, according to Fitch, Moody’s, and S&P, but instead regard both them and Russian capital inflows as a structural shift. Both workers and capital have remained much longer than expected.

Lastly, in the frontier market space—defined as small, developing economies with investable stock markets—many of Georgia’s peers are regarded as much more likely to face sovereign refinancing challenges and currency pressures. That is how investors are analyzing the situation when making their spreadsheet-driven decisions. Currently, emerging and frontier markets are generally in favor, and Georgia’s growth rates make it especially attractive.

International markets generally view Georgia’s management of inflation favorably, praising the central bank for its proactive, data-driven approach to maintaining price stability amid high external shocks. Despite annual inflation hitting 5.9% in April 2026—driven by external food and oil prices and regional volatility—investor confidence remains solid, evidenced by successful Eurobond rollovers.

The next frontier: China and Asian capital

To keep foreign money flowing in, Georgia is planning its next major move to reach Asian investors, targeting them with large-scale issuances of government lari bonds this spring, according to Finance Minister Lasha Khutsishvili. Timing is favorable, as China seeks to diversify its foreign financial holdings away from the U.S. and Europe. There is already a strong relationship: the Industrial and Commercial Bank of China was one of the lead managers in the government’s January Eurobond issue. Georgia has also taken steps to remove technical barriers for Chinese funds, and in February it gained access to the China Interbank Bond Market. Further facilitating international financial flows, the National Bank has created financial infrastructure that integrates local lari markets—for corporate as well as government bonds—with global financial hubs.

Asian investors are increasingly seeing Georgia as a stable emerging market, particularly relative to broader global uncertainty, and its sovereign debt as a proxy for betting on the Middle Corridor trade route through which Chinese goods access Europe and, en route, the growing Central Asian markets.

Given the crisis in international shipping markets, investors are willing to overlook, for now, challenges such as Caspian port bottlenecks—as described by Levan Lomsadze, founder of GEORAIL Consulting on BM.ge—and Georgian Rail’s need for hundreds of millions of dollars in investment. Currently, the Georgian route is the only one with fully operational infrastructure despite Armenia’s efforts to offer an alternative via the “Trump Corridor.” Georgian cargo volumes reached record highs in early 2026.

Building the infrastructure for global investment

But the real key to this newfound international confidence in Georgian paper has been the early 2026 move by the NBG to collaborate with Bloomberg and ICE (the Intercontinental Exchange) to publish seven Georgian Government Bond Indices on these global platforms. This makes Georgian securities transparent and accessible to international investment and pension funds, providing an internationally recognized benchmark for evaluating risk and yield.

The indices, developed with IMF technical assistance, allow foreign investors to analyze Georgian securities using familiar, high-transparency methodology. This move removed a major barrier to entry for foreign institutional investors, facilitating the structuring of exchange-traded funds (ETFs) and strengthening investor confidence.

With regard to China, the most critical move is Georgia’s direct entry into the China Interbank Bond Market (CIBM), which signals to Chinese state and private investors that Georgia is a sophisticated, “China-ready” financial partner. In February 2026, the National Bank of Georgia opened accounts with the People’s Bank of China (PBOC). This allows the NBG to trade and settle in Chinese government bonds, a move intended to encourage reciprocal investment from Chinese institutional players into Georgian debt. Four Georgian banks had applied for direct membership in the Cross-Border Interbank Payment System (CIPS) as of March 2026. This reduces reliance on SWIFT for yuan-denominated trades, lowering transaction costs and risks for Chinese investors.

Pursuing further important Asian links, this time with the major Asian financial center of Singapore, the National Bank organized a landmark summit last October with the country’s Global Finance and Technology Network (GFTN). This launched Georgia’s official entry into the global GFTN network, an initiative originating from the Monetary Authority of Singapore (MAS) to link emerging financial hubs. Strategies were discussed to modernize trade financing and cross-border payments along the Middle Corridor trade route linking Asia and Europe.

As of last month, the outlook for Georgian bonds through the remainder of 2026 and into 2027, in the eyes of local investment banks Galt & Taggart and TBC Capital, was generally stable to positive, supported by strong economic growth projections, robust foreign exchange reserves, and successful liability management. Although this is tempered by geopolitical risks and a moderation in economic growth compared to the 2024–2025 period, the numbers are telling a story that foreign investors like.